Global hydraulic fracturing market value is set to step from a USD 58.5B 2025 estimate to a USD 63.2B 2026 forecast, en route to USD 93.9B by 2033, a trajectory that translates directly into demand for high-pressure fracturing pumps, wellhead valves and the steel tube inventory that feeds them [S2].

That single oilfield data point is the dominant macro driver for 2026 industrial hydraulics: shale gas, tight gas and tight oil applications are forecast as the largest end-use cluster, with plug-and-perf and sliding-sleeve technologies splitting the stimulation architecture [S2]. Adjacent segments — elevators, dump-trailer telescopic cylinders, mobile power units — run on the same supply chain of honed tubes, chrome-plated rods, cartridge valves and gear pumps, which is why 2026 procurement calendars are being written around the same delivery slots.

Demand Stack: Where the Volume Actually Lands in 2026

The fracturing segment alone accounts for tens of billions of dollars of pump, blender and high-pressure manifold spend in 2026, with the technology split between plug-and-perf and sliding sleeve completions and the material split between corrosion-resistant alloys and standard carbon-steel tubulars [S2].

North America remains the largest regional block, followed by Asia Pacific and the Middle East & Africa, while Europe retains a process-industry floor — presses, injection moulding clamp cylinders, marine deck machinery — that does not move with rig count [S2]. Sourcing teams report that the elevator and dump-trailer telescopic cylinder lines in China, such as the Hanzhuoli Hydraulic Technology (Jinan) Co. operation that builds dump-trailer telescopic cylinders, scissor-hoist lifts and hydraulic power units, are running at capacity to backfill mobile-equipment demand even as the oilfield orderbook is being re-cut by every USD 5B swing in the fracturing forecast [S3]. The knock-on effect is visible in pneumatic conveying and cylinder sizing, where the same forged-body component base is being reallocated between pneumatic and hydraulic work.

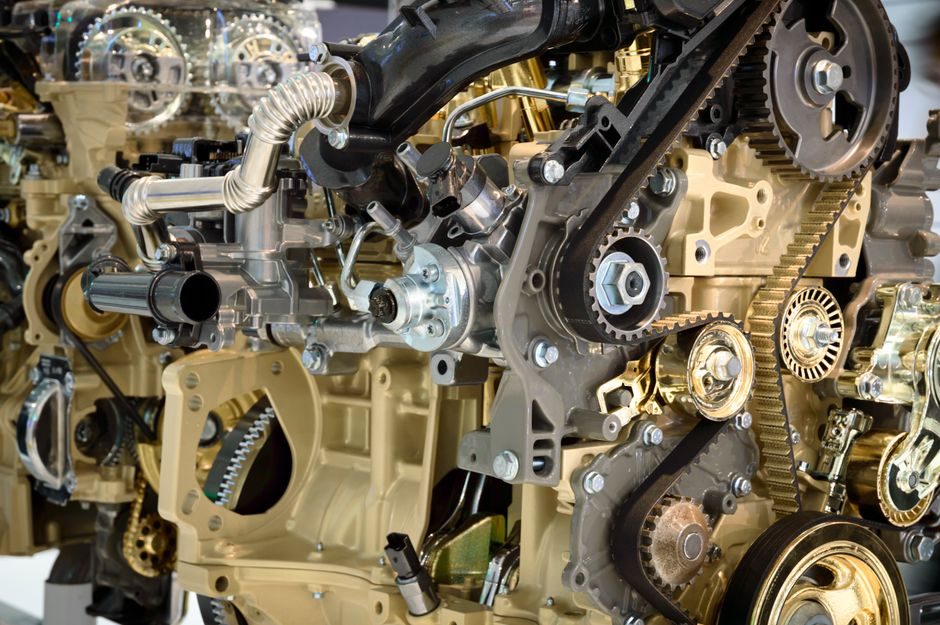

Component Stack: Pumps, Cylinders, Motors, Valves, Power Units

At component level, a 2026 hydraulic system is a stack of five building blocks: a hydraulic pump (gear, vane, piston or bent-axis), a hydraulic motor (orbital, gerotor, axial-piston, radial-piston) for rotary output, a hydraulic cylinder (tie-rod, welded, telescopic) for linear output, a hydraulic valve (directional, pressure, flow, proportional) for control, and a hydraulic power unit that integrates reservoir, filtration, motor-pump coupling, cooling and instrumentation. [S1]

Each block is now being specced against tighter envelopes: piston pumps for fracturing typically run 300–500 hp per stage at working pressures in the 5,000–10,000 psi window, while mobile-equipment piston pumps on dump trailers and refuse trucks sit closer to 3,000–5,000 psi with load-sensing modulation [S2]. Cylinder-side, the telescopic-dump format is the volume leader in mobile hydraulics and is built around multi-stage honed tubes with stage diameters stepped by 20–40 mm; welded-body cylinders dominate industrial presses and marine gear [S3]. Valve architectures continue to migrate from on/off solenoid blocks to load-sensing and proportional architectures, with cartridge valves absorbing flow rates to 200–400 L/min per section on mobile machines.

Spec Levers Process Engineers Are Negotiating in 2026

Four spec levers dominate 2026 procurement conversations: pressure rating, corrosion package, filtration class and electronic interface. Pressure rating is the first gate — specifying 350 bar instead of 210 bar on a hydraulic cylinder doubles the wall thickness of the barrel and the rod diameter, which has direct consequences for the supply of 27SiMn, 45# and 40Cr honed tubes that Chinese telescopic-cylinder lines such as the Jinan-based Hanzhuoli operation draw on [S3].

Corrosion package decisions — zinc-rich primer, e-coat, powder top-coat, stainless fittings, nitrile versus FKM seals — are increasingly written into the RFQ rather than negotiated at order acceptance, because mobile-equipment fleets are pushing warranty terms past the 24-month mark. Filtration class is the third lever, and the 2026 default for new mobile and industrial builds is ISO 4406 cleanliness codes in the 18/16/13 to 20/18/15 band with in-line beta-rated elements. The fourth lever is electronic interface: CAN J1939, CANopen and IO-Link gateways are now standard bid lines, while 4–20 mA plus HART remains the dominant protocol on process-industry hydraulic valve positioners and hydraulic actuator controllers in chemical and oil & gas skids.

Material & Manufacturing Stack: Forgings, Castings, Honed Tubes, Chrome-Plated Rods

Raw-material flow is the binding constraint underneath all five component blocks. Cylinder barrels are cut from cold-drawn seamless tube (16Mn, 25Mn, 27SiMn) and honed to ISO 4394-1 surface finishes typically held between Ra 0.2–0.4 µm, while piston rods are medium-carbon 45# steel, induction-hardened and chrome-plated to 0.020–0.030 mm with hard-chrome bath processes that are themselves under environmental review in the EU and China [S3].

Valve bodies and pump housings split between nodular cast iron (QT450-10, QT600-3) for medium-pressure work and forged 42CrMo / 20CrMnTi for high-pressure blocks, with the forging-versus-casting decision driven by lot size and pressure rating. For mobile-equipment telescopic lines, the cost stack is dominated by stage machining and assembly labour rather than raw steel, which is one reason Chinese suppliers such as the Jinan dump-trailer cylinder operation can ship FOB at price points that EU forging shops cannot meet without automation [S3]. Process engineers should expect a parallel argument on forged components in adjacent industries — see the bearing supplier-tier debate — where forging, heat-treatment and grinding capacity is the real bottleneck.

Comparison: Industrial vs Mobile vs Oilfield vs Elevator Hydraulics

Four operating envelopes are useful to compare directly, because the components cross over but the duty cycles do not: industrial presses typically run at 160–250 bar with ISO VG 32–46 mineral oil, continuous duty at 40–60 °C; mobile construction and dump-trailer systems run at 200–350 bar with ISO VG 32–46, intermittent duty with cold-start swings from –20 °C to +80 °C; oilfield fracturing systems run at 350–700 bar (5,000–10,000 psi) with high-VI hydraulic fluid and water-glycol mixes, near-continuous duty at elevated ambient; and hydraulic elevators operate at 40–80 bar with low-noise gear pumps and soft-start valve packages, short-duty with frequent stops [S1][S2][S3].

Against those envelopes, the component spec diverges: industrial presses use tie-rod cylinders and inline piston pumps; mobile equipment uses welded or telescopic cylinders, axial-piston pumps, and load-sensing valves; oilfield systems use super-quenched piston pumps, high-pressure fracturing iron rated to 15,000 psi test, and accumulator-backed pressure control; elevators use low-RPM gear pumps, Vickers vane stacks, and oversize reservoirs for thermal stability [S1][S2]. The practical sourcing consequence is that a hydraulic power unit built for elevator duty is not a drop-in for a fracturing feed line, even if the reservoir and the motor look superficially similar.

Failure Modes & Constraints Engineers Are Watching in 2026

Three failure modes are driving warranty spend in 2026. First, seal blow-by in high-pressure cylinders, almost always traceable to rod-surface roughness excursions or chrome-plating porosity above Ra 0.4 µm; second, cavitation pitting in piston pumps feeding cold-start mobile circuits below 5 °C; third, valve-spool sticking in proportional and load-sensing architectures, normally linked to fluid cleanliness worse than ISO 4406 20/18/15 or to varnish build-up from high-temperature reservoir operation above 80 °C. [S2]

Beyond those, supply-side constraints continue to bite: honed-tube and chrome-plated-rod capacity in China is being absorbed by dump-trailer, refuse-truck and tipping-trailer telescopic-cylinder lines, which is one reason single-source risk on hydraulic cylinder bodies is being re-rated by European OEMs [S3]. For a sense of the macro materials pressure on parallel supply chains, see the cobalt supply–demand gap note and the natural gas power-switching dispatch piece — both are downstream of the same industrial-throughput throttle.

Standards, Sourcing Signals and What to Track Next

Specifying engineers in 2026 are working against a familiar standard stack: ASME B30 for cable and crane hydraulics, ISO 4413 for hydraulic fluid power general rules, ISO 4414 for pneumatic-fluid-power logic, ISO 6020 for cylinder dimensions, ISO 4391 for performance, ISO 4406 for fluid cleanliness, ISO 6149 for tube fittings, and API Specs for oilfield wellhead and fracturing equipment, with the fracturing market's 2026 baseline of USD 63.2B framing the OEM-versus-aftermarket split [S2].

and its peers continue to push capacity into dump-trailer and scissor-hoist builds [S3]. For adjacent demand context, the cable and wire forecast and the pneumatic systems valve-architecture note track the same copper-and-steel macro pulse that the hydraulic industry is riding into 2026.