Machine tool smart manufacturing in 2026 is defined less by the spindle and more by the data spine connecting it: Industrial Internet of Things (IIoT) sensors on spindles, ball screws, and coolant manifolds feed condition-monitoring platforms that flag tool wear and thermal drift before scrap is produced [S2].

The 2026 sourcing map is anchored by a China powertrain-automation cluster with engineering roots in the former Dalian Machine Tool Institute and Yida Daying, offering turnkey smart-manufacturing system integration for transfer lines, robotic loaders, and AGV-linked FMC pools [S1]. Procurement teams running global plant rollouts will also be weighing the December 2026 Manufacturing Indonesia / Machine Tool Indonesia / Industrial Automation Indonesia co-located shows at JIEXPO Kemayoran (2–5 December 2026) as a Southeast Asia sourcing gate [S4].

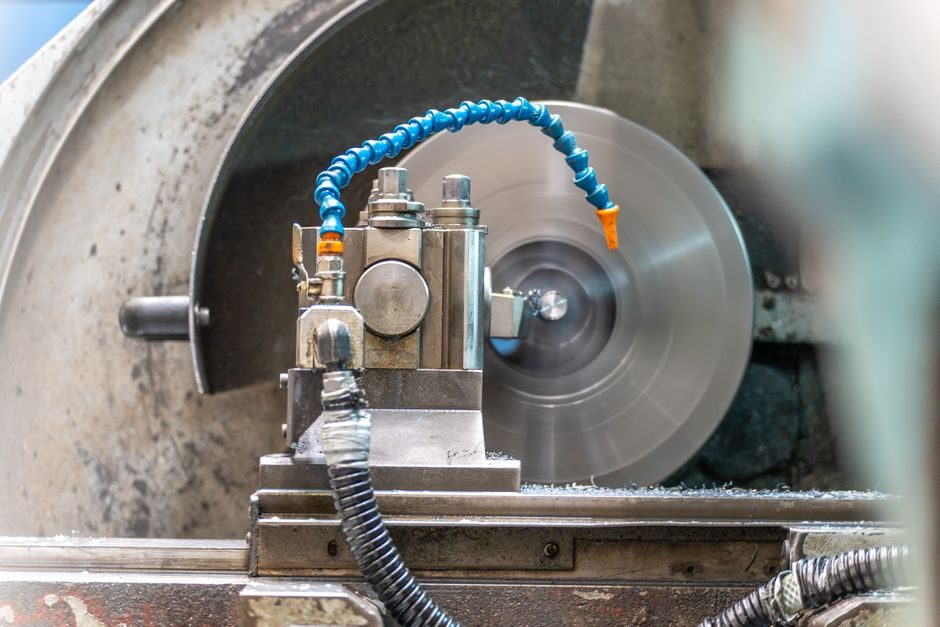

What "Smart Manufacturing" Actually Means on a CNC Shop Floor

The IBM definition of smart manufacturing, last updated 2023, is the operational baseline most 2026 integrators still quote: highly integrated IIoT sensing feeding centralized analytics over real-time machine health, energy, and process data [S2]. On a CNC cell this maps to four concrete layers — spindle vibration and load sensors, linear-scale thermal compensation drives, edge controllers running OPC UA, and MES-level dispatching. None of these layers is optional in a 2026 spec: vendors that ship a new VMC without OPC UA, MTConnect, or a documented MQTT/AMQP southbound interface are routinely rejected at RFQ stage by automotive Tier-1 buyers.

The 2026 China-supplier catalog reinforces the practical layer: BT40, HSK63, and HSK100 tool-holder interfaces, balanced-end-mill holders in the US$13.00–13.99 per-piece range, and QGG50 / QKG50 / GT precision vises at US$25.89–35.89 [S3]. These are the workholding and tooling standards a smart cell must natively index against, not a retrofit bolt-on. For a deeper parallel on automation cells outside the metalcutting world, the mining-equipment automation snapshot for 2026 shows the same IIoT-data-spine pattern applied to mobile equipment telematics.

Selection Criteria for a 2026 Smart Machine-Tool Cell

Specifying engineers should score each candidate on six concrete criteria before any commercial negotiation, in this order: (1) controller openness — OPC UA, MTConnect, and a documented SDK; (2) drive architecture — closed-loop servo with absolute linear scales, not open-loop stepper; (3) tool interface — HSK63A as the 2026 default for 5-axis cells, HSK100 for heavy-duty milling, BT40 retained for cost-sensitive 3-axis VMCs [S3]; (4) pallet pool and AGV interface — electrical and protocol conformance to the existing line; (5) spindle health sensing — vibration, load, temperature, all streamed to the same analytics platform; (6) integrator track record in the specific commodity (powertrain, gearbox housing, EV battery tray).

The China powertrain-automation integrator profile is unusually concentrated: the lead engineering staff of the firm in [S1] were trained at the Dalian Machine Tool Institute and Dalian Machine Tool Plant, and from Yida Daying Machine Tool — three of the historic pillars of Chinese heavy-cut powertrain lines. For buyers whose bottleneck is powertrain-cell throughput rather than general part-machining, that pedigree is the single most predictive spec on the vendor shortlist. Buyers running mixed-load plants that include material handling, overhead cranes, and cell-side workstations will find the single-girder crane supplier map for 2026 a useful parallel on how China cluster sourcing gates now structure capital-equipment buys.

Who Smart-Cell Automation Is For — and Who It Is Not For

Smart-cell automation pays back inside 18–30 months on three profile types: high-mix/high-volume powertrain families (engine blocks, transmission housings, EV reducers), medical implants and aerospace structural parts that require documented process capability, and Tier-1 automotive lines with annual volumes above roughly 50,000 identical workpieces per cell. It is a poor fit for job shops running batch sizes below 200 pieces per setup, R&D prototyping where fixture design dominates cycle time, and any plant whose existing controller fleet is still a closed proprietary stack without OPC UA export — the retrofit cost will exceed the IIoT benefit. [S1]

A practical "do not automate" signal in 2026: a plant where the average operator still hand-writes setup sheets, where tooling is bar-coded only informally, and where the only network is office Wi-Fi extending into the shop. Smart cells fail not on sensors but on the data hygiene underneath them. Plants that need a lower-stakes entry point are usually better served by retrofittable spindle-current and tool-wear sensors bolted onto existing CNCs, not a full line rebuild.

Criteria-Based Comparison: Smart-Cell Stack Options in 2026

Four smart-cell stack options dominate 2026 RFQs. (1) Premium Western OEM turnkey (e.g. DMG MORI, Mazak, GF): strongest controller integration, highest price, 12–18 month lead time on full lines. (2) Japan/Korea OEM + Western analytics (Okuma, Doosan, Hyundai Wia with third-party IIoT): strong spindle reliability, mid-price, 8–14 month lead time. (3) China OEM + China integrator (Shenyang, Dalian, SMTCL, with an integrator staffed from the former Dalian Machine Tool Institute lineage) [S1]: most aggressive price-per-station, 6–10 month lead time, requires rigorous FAT/SAT and protocol conformance testing. (4) Retrofit IIoT layer on existing fleet (Senseye, Augury, MachineMetrics-class platforms) [S2]: lowest capex, fastest ROI, but no improvement in chip-to-chip time.

Selection decision rule: choose (4) if capex is rationed and the existing fleet is under-instrumented; choose (3) if the plant is a greenfield China-region build with a powertrain focus; choose (2) for a brownfield brownfield-plant upgrade in a global footprint; choose (1) only for aerospace/medical or where the OEM's brand itself is on the bill of materials. Across all four, the protocol test gate is identical: must publish OPC UA companion spec, must expose MTConnect over TCP, must allow direct read of spindle load, axis position, and alarm history without a vendor cloud dependency.

Real Use Cases: What Buyers Are Actually Funding in 2026

The dominant 2026 use case is the EV reducer cell: a 5-axis HSK100-equipped horizontal machining center with pallet pool, automated deburring station, and in-line gear-measurement probing, all linked by AGV to a heat-treatment and assembly line. The China powertrain-automation cluster has pitched this exact topology with engineering staff out of the Dalian and Yida Daying lineage [S1]. A second use case is the contract-manufacturer Tier-1 cell: an automotive Tier-1 running mixed-model transmission housings, where the same HMC platform is re-fixtured robot-side for a new part number within 90 seconds. A third, more conservative use case, is the retrofit bolt-on: a 2018-era VMC fleet fitted with spindle-current and vibration sensors feeding the IBM-style IIoT platform described in [S2], giving a 6-month payback through tool-life extension alone.

A typical 2026 cell spec sheet runs: 12,000 rpm direct-drive spindle, HSK63A taper on the 5-axis head, 30-tool chain magazine, pallet size 400 × 400 mm, Siemens SINUMERIK ONE or FANUC 31i-MB5 controller with OPC UA server active by default, AGV interface per the VDMA 4050 profile, and a vibration / load / temperature sensor pack on each linear axis. Buyers running parallel capex plans on the same site — overhead material handling, workholding, and station-side hoists — will find the single-girder crane sizing and selection guide for 2026 a useful adjacent reference.

Limitations, Failure Modes and Sourcing-Show Timing

The biggest 2026 failure mode on smart-cell projects is not the robot or the controller, it is the integration layer: protocol-conformance gaps between the cell PLC and the plant MES, under-specified network cabling, and a 5G/Wi-Fi dead zone at the AGV turning radius. The second failure mode is the data-sovereignty gap: many Western buyers now reject any smart-cell stack whose analytics platform cannot run on-prem, citing export-control and plant-cybersecurity rules. The third is integrator attrition: China cluster integrators staffed from the Dalian Institute and Yida Daying lineage [S1] have strong engineering depth, but the firm-level track record is short, so warranty and post-FAT support contracts need to be locked in writing before down-payment.

For 2026 sourcing, two timing gates matter. The first is the December 2026 JIEXPO cluster in Jakarta (2–5 December 2026) — Manufacturing Indonesia, Machine Tool Indonesia, Industrial Automation Indonesia, Tools & Hardware Indonesia, and Production Logistics Indonesia run as a single co-located show, with a 2026 expansion into food manufacturing and plastics packaging adjacencies [S4]. The second is the OEM internal review cycle: most China integrators require a 90-day FAT window plus a 60-day SAT, so RFQs in Q3 2026 are the latest realistic entry point for a Q3 2027 line hand-over. Buyers sourcing the auxiliary equipment that sits around the cell — cranes, vises, workholding, wear parts — should plan their parallel RFQs to close inside the same calendar window.

Trackable signals worth watching through the rest of 2026: the published exhibitor list for the December 2026 Jakarta cluster [S4], any OPC UA Companion Specification update for machine tools from the VDMA, and the next round of capacity announcements from the China powertrain-automation cluster anchored on the Dalian / Yida Daying engineering lineage [S1].

For component-level specifications, see additive manufacturing material, smart camera, and smart meter.